“월세만 카드결제 안 된다는 건 이상하지 않아요?”

여의도역 앞의 한 카페. 약속 시간보다 10분 일찍 도착한 김기태(32) 데브디 대표는 노트북을 펼쳐놓고 무언가를 집중해서 보고 있었다. “오전에 새로운 제휴 건이 들어와서요.” 화면에는 월별 거래 현황을 보여주는 대시보드가 떠 있었다. 수치들이 가파르게 상승하는 그래프가 눈에 띄었다.

“6개월 전만 해도 이 정도 성장을 예상하지 못했어요. 솔직히 말하면, 마지막 도전이다 생각하고 시도 했죠.”

김기태 대표가 창업한 데브디의 주력 서비스 ‘집업페이’는 1인가구 올인원 솔루션 ‘집업’앱 내에 있는 월세 카드 결제 솔루션이다. 2023년 앱 출시 이후 수익화를 고민하던 그가 내놓은 서비스이다. 집업페이는 작년 10월 출시 이후 6개월 동안 매 달 거래액이 150% 씩 성장 중이다.

긴 자취 생활에서 찾아낸 창업 동기

월세를 카드로 내는 과정이 왜 어려운지 묻자, 그는 “생각보다 복잡하다”고 털어놨다.

“임대인 대부분이 개인이라 카드 결제를 받으려면 세금 문제 때문에 꺼린다”는 것. 결국 세입자는 매달 현금으로 송금해야 하고, 이 과정에서 아무런 혜택을 얻을 수 없다.

김기태 대표 역시, 10여년간 타지에서 혼자 살면서 같은 경험을 했다. “월세 내는 날이 카드값 빠져나가는 날과 겹치거나, 갑자기 큰 지출이 생기면 돈 관리가 어려웠죠. 그 때마다 ‘월세도 카드처럼 결제일과 출금일 사이에 여유가 있으면 편할 텐데’라는 생각을 했습니다.”

김기태 대표는 영국에서 AI 차 큐레이션 스타트업 ‘DiversiTea’를 창업한 경험이 문제 해결의 열쇠였다고 했다. “불가능해 보이는 문제도 단계별로 쪼개면 해결책이 나온다”는 것. 특히, Monzo나 Revolut, Wise와 같은 선진 핀테크 스타트업의 서비스를 재밌게 보던 경험에서, 이런 아이디어를 생각해낼 수 있었다.

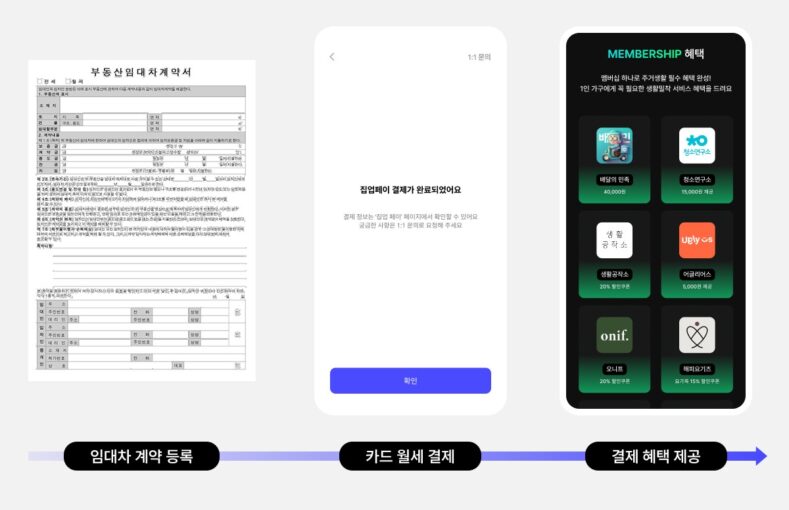

“기존에도 월세의 카드 결제가 불가능한 건 아니었어요”. 김기태 대표에 따르면, 기존에는 임대인이 직접 카드기를 가지고 결제 받거나, 서면으로 동의해준 임대인에 한해 금융사의 혁신금융 서비스로 진행할 수 있었다. 하지만 “거주 중인 월세 집주인의 연세가 90대이다. 이를 쉽게 이해하지 못한다”면서, 임대인 비개입형 구조의 효과성을 설명했다. 집업페이는 PG사를 중간에 끼어, 임차인의 송금을 대신 처리하는 구조이다.

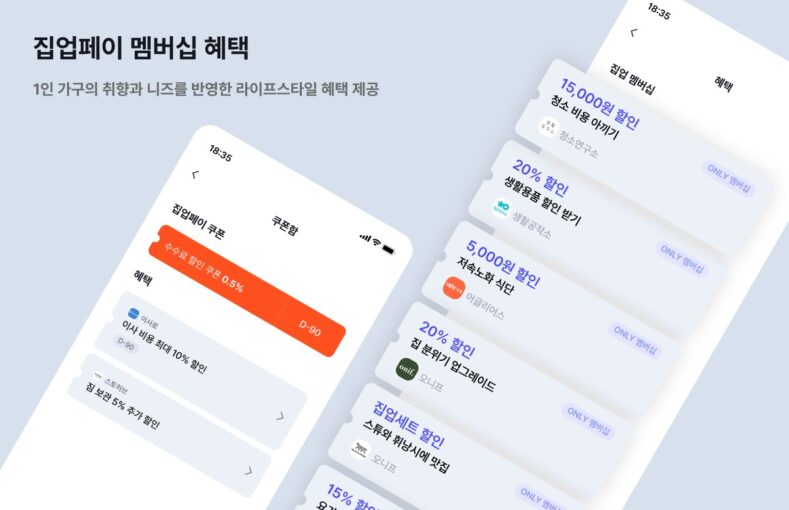

“사용자는 집업에서 본인의 임대차 계약서를 인증하고, 월세를 카드로 결제합니다. 월세 금액으로 카드 실적을 쌓는 것은 물론, 포인트나 결제일 조정같은 카드 혜택에 세액공제, 주거·라이프스타일 멤버십 혜택도 함께 누릴 수 있어요. 임대인은 기존과 똑같이 월세를 받게 되고요.”

평균 연령 26.8세, 2030 세대가 빠르게 반응

집업페이 사용자의 평균 연령은 26.8세이다. 다양한 카드 사용에 익숙하고, 각종 혜택에 민감한 세대다. 김기태 대표는 “자연스럽게 그렇게 됐다”고 했다. “기성세대는 월세를 현금으로 내는 게 당연하다고 생각하는데, 젊은 세대는 ‘왜 월세 납부만 현금이어야 해’라고 의문을 가지거든요.”

마케팅은 쉽지 않았다. ‘카드로 월세를 낸다’는 개념이 아직 낯설고, 어색하다는 이들이 여전히 많다. 일부는 ‘카드깡’과 혼동하는 부정적인 인식을 갖기도 한다. 그래서 보안과 안정성 확보에 집중했다. 데브디는 업계 최초로 ISO 9001과 ISO 27001을 동시에 획득하며, 안정적이고 신뢰할만한 서비스 운영 체계를 갖췄다.

전세사기 방지에서 월세 금융까지

집업페이는 처음부터 주력 사업이 아니었다. 집업의 통합 서비스 전략은 1인 가구가 주거 생활에서 겪는 파편화된 문제들을 하나의 플랫폼에서 해결하자는 철학에서 출발했다. 이사 준비부터 마무리까지 전 과정을 관리할 수 있는 ‘이사플래너’와 개인 맞춤형 매물 탐색 기능으로 시작해, 이후 전세사기 예방을 위한 ‘전세안전리포트’, 1인 가구 특화 정보를 담은 ‘매거진’ 등으로 범위를 확장해왔다.

“사용자들이 이사와 관련된 전 과정에서 여러 도움을 받고 싶어 한다는 걸 알게 됐어요. 집 구하기와 계약서 검토, 이사 준비, 그리고 매달 월세 내기까지. 이 중에서도 특히 월세가 반복적이고, 불편함이 컸죠. 그래서 여기에 집중하게 됐습니다”

수익 모델은 3가지, 데이터 협업이 핵심

이런 1인가구 토탈 올인원 서비스를 지향하는 집업의 수익원은 세 가지다. 카드 결제 수수료와 이사·청소·수리 등 주거 관련 제휴 서비스 수익, 그리고 금융기관 협업을 통한 제휴카드 및 맞춤형 금융 상품에서 발생하는 수익이다.

그는 “여러 금융기관과의 협업을 통해 1인 가구에 특화된 금융 상품을 확장 중”이라고 설명했다.

“작년 하나은행, 하나카드와 협업을 진행했어요. 하나카드는 제휴카드를 설계해 만들기도 했죠.”

올해는 우리금융그룹과 카카오뱅크, BNK경남은행 등 오픈 이노베이션 사업을 진행하며 다양한 형태의 협업을 진행하고 있다.

김기태 대표는 집업의 비전을 “월세를 단순한 지출이 아니라, 개인의 금융 생활을 시작하는 첫걸음으로 바꾸는 것”이라고 했다. 매월 반복되는 월세 납부를 고정비로만 인식하는 것이 아니라, 신용도 관리, 포인트 적립, 투자 연계 등 다양한 금융 혜택과 연결해 임차인 재무 설계와 금융 포트폴리오 확장을 가능하게 하는 구조를 지향한다. 1인 가구가 주거비 지출에서도 실질적 경제적 이익을 얻을 수 있도록 돕는 것이 방향이다.

비록 금융회사는 아니지만, 데브디는 사용자 입장에서 금융을 쉽게 만들고자 한다. 기술은 사람들의 일상 속 돈의 흐름을 보다 유연하게 바꾸는 데 초점을 맞추고 있다.

월세의 카드 지불이 상식인 세상

유사 서비스를 펼치는 타사에 대해서는 “집업페이의 차별화된 강점이 있다”고 강조했다. 업계 최저 수준의 수수료와 금융권 제휴카드, 주거 생활 전반을 아우르는 멤버십 서비스 등 혜택을 통해 유저에게 더 나은 선택지와 가치를 제공한다.

그는 “월세를 카드로 지불한다는 개념이 익숙하지 않지만, 이제 자금 관리 수단으로 관심 갖는 이들이 늘고 있다”며 “집업페이로 월세 가구가 주거비 지출에서 다양한 금융 이익을 만들도록 돕고 싶다”고 말했다.

월세를 ‘현금만’ 내던 시대는 서서히 저물고 있는 것 같다.

김기태 데브디 대표는 영국 The University of Sheffield를 졸업하고, 영국에서 AI 기반 커머스 스타트업 DiversiTea를 창업했다. 이후 소셜벤처 액셀러레이터 언더독스에서 코치로 활동하며 다양한 창업팀을 멘토링했다. 2022년 데브디를 창업해 ‘집업x을 론칭한 이후, 현재까지 4만 명 이상의 사용자를 확보했다.

CEO Kim Ki-tae makes the impossible of ‘paying rent by card without landlord’ a reality

“Isn’t it strange that only monthly rent cannot be paid by credit card?”

A cafe in front of Yeouido Station. Kim Ki-tae (32), CEO of Devdi, who arrived 10 minutes earlier than the appointed time, was concentrating on something with his laptop open. “A new partnership came in this morning.” A dashboard showing the monthly transaction status was displayed on the screen. A graph with numbers rising steeply caught my eye.

“Even six months ago, I wouldn’t have expected this level of growth. To be honest, I thought of it as my last challenge.”

The main service of Devdi, founded by CEO Kim Ki-tae, is the monthly rent card payment solution within the 'Zipup' app, an all-in-one solution for single-person households. It is the service that he came up with while contemplating monetization after the app's launch in 2023. Since its launch in October of last year, Zipup Pay has been growing its monthly transaction amount by 150% for the past six months.

Motivation for starting a business discovered through long-term living alone

When asked why the process of paying rent by card was difficult, he confessed, “It’s more complicated than I thought.”

“Most landlords are individuals and are reluctant to accept card payments due to tax issues.” In the end, tenants have to send cash every month, and there is no benefit to be gained from this process.

CEO Kim Ki-tae also had the same experience while living alone in a foreign country for over 10 years. “When the day I had to pay my rent overlapped with the day my credit card bill was deducted, or when I suddenly had a big expense, it was hard to manage my money. Every time, I thought, ‘It would be easier if there was some time between the payment date and the withdrawal date, like with a credit card.’”

CEO Kim Ki-tae said that his experience in founding the AI tea curation startup 'DiversiTea' in the UK was the key to solving the problem. "Even problems that seem impossible can be solved by breaking them down into steps." In particular, he was able to come up with this idea from his experience of enjoying the services of advanced fintech startups such as Monzo, Revolut, and Wise.

“It wasn’t impossible to pay rent with a card before.” According to CEO Kim Ki-tae, previously, landlords could receive payments directly with a card machine, or only landlords who gave written consent could use innovative financial services from financial institutions. However, he explained the effectiveness of a structure that does not involve landlords, saying, “The current monthly rent landlord is in his 90s. It’s hard for them to understand this.” Zipup Pay is a structure that processes the tenant’s remittance on their behalf by intervening with a PG company.

“Users authenticate their lease agreements at the home and pay their monthly rent with a card. In addition to accumulating card performance with the monthly rent amount, they can also enjoy card benefits such as points and payment date adjustments, tax deductions, and housing/lifestyle membership benefits. The landlord receives the monthly rent as before.”

Average age 26.8 years old, 2030 generation responds quickly

The average age of the Zipup Pay users is 26.8 years old. They are a generation accustomed to using various cards and sensitive to various benefits. CEO Kim Ki-tae said, “It just happened naturally.” “The older generation thinks it is natural to pay the monthly rent in cash, but the younger generation wonders, ‘Why should only the monthly rent be paid in cash?’”

Marketing was not easy. There are still many people who are unfamiliar with the concept of 'paying rent with a card' and find it awkward. Some people have a negative perception of it, confusing it with 'card fraud'. So we focused on ensuring security and stability. Devdi was the first in the industry to simultaneously obtain ISO 9001 and ISO 27001, and established a stable and reliable service operation system.

From preventing fraud to monthly rent financing

Zipup Pay was not the main business from the beginning. Zipup’s integrated service strategy started from the philosophy of solving the fragmented problems that single-person households experience in their residential life on a single platform. It started with the ‘Moving Planner’ that can manage the entire process from moving preparation to completion and the personalized property search function, and later expanded the scope to include the ‘Rental Safety Report’ to prevent rental fraud and the ‘Magazine’ containing information specialized for single-person households.

“We found that users wanted help with all aspects of moving. From finding a home, reviewing contracts, preparing for the move, to paying the monthly rent. Of these, monthly rent was particularly repetitive and inconvenient. That’s why we focused on this.”

There are three revenue models, and data collaboration is key.

The revenue sources of this one-person household total all-in-one service are threefold: card payment fees, revenue from housing-related affiliate services such as moving, cleaning, and repairs, and revenue from affiliate cards and customized financial products through collaboration with financial institutions.

“We are expanding financial products tailored to single-person households through collaboration with various financial institutions,” he explained.

“Last year, we collaborated with Hana Bank and Hana Card. Hana Card also designed and created a partnership card.”

This year, we are conducting open innovation projects with Woori Financial Group, Kakao Bank, and BNK Gyeongnam Bank, and are carrying out various forms of collaboration.

CEO Kim Ki-tae said that the vision of the company is “to change monthly rent from a simple expense to the first step in starting a personal financial life.” Rather than recognizing the monthly rent payment as a fixed cost, the company aims to connect it with various financial benefits such as credit management, point accumulation, and investment linkage to enable tenant financial planning and financial portfolio expansion. The goal is to help single-person households obtain real economic benefits from their housing expenses.

Although not a financial company, Devdi aims to make finance easier for users. The technology focuses on making the flow of money in people’s daily lives more flexible.

A world where paying rent by credit card is common sense

Regarding other companies that provide similar services, he emphasized that “Zipup Pay has a differentiating strength.” It provides better choices and value to users through benefits such as the industry’s lowest commissions, financial sector affiliated cards, and membership services covering all aspects of residential life.

He said, “The concept of paying rent with a card is unfamiliar, but more and more people are becoming interested in it as a means of managing their finances,” and “I want to help renters generate various financial benefits from their housing expenses through Zipup Pay.”

It seems that the era of paying monthly rent 'only in cash' is slowly coming to an end.

Kim Ki-tae, CEO of Devdi, graduated from The University of Sheffield in the UK and founded DiversiTea, an AI-based commerce startup in the UK. He then worked as a coach at social venture accelerator Underdogs and mentored various startup teams. Since founding Devdi in 2022 and launching 'Zipupx', it has secured over 40,000 users to date.

「賃貸人の同意なしに、カードで家賃を払う」という不可能を現実に、キム・ギテ代表

「月税だけカード決済できないというのはおかしくないですか?」

汝矣島駅前のカフェ。約束時間より10分早く到着したキム・ギテ(32)デブディ代表はノートパソコンを広げて何かを集中して見ていた。 「午前に新たな提携件が入ってきます」画面には毎月の取引状況を示すダッシュボードが浮いていた。数値が急上昇するグラフが目立った。

「6ヶ月前だけでもこれほど成長を予想できませんでした。正直に言えば、最後の挑戦だと思って試してみました。」

キム・ギテ代表が創業したデブディの主力サービス「集業ペイ」は、1世帯のオールインワンソリューション「集業」アプリ内にあるウォルセールカード決済ソリューションだ。 2023年アプリ発売以来収益化を悩んでいた彼が出したサービスだ。集業ペイは昨年10月発売以来6ヶ月間毎月取引額が150%ずつ成長中だ。

長い跡の生活で見つけた創業動機

家賃をカードで出す過程がなぜ難しいのか尋ねると、彼は「考えより複雑だ」と打ち明けた。

「賃貸人の大部分が個人であり、カード決済を受けるには税の問題のために消極的」ということ。結局、テナントは毎月現金で送金しなければならず、この過程で何の恩恵を受けることもできません。

キム・ギテ代表もやはり、10余年間、タージで一人暮らしで同じ経験をした。 「月税の出る日がカード値抜けていく日と重なったり、突然大きな支出ができればお金の管理が難しかったです。

キム・ギテ代表はイギリスでAI車キュレーションスタートアップ「DiversiTea」を創業した経験が問題解決の鍵だったという。 「不可能に見える問題も段階別に割れば解決策が出てくる」ということ。特に、MonzoやRevolut、Wiseのような先進のフィンテックスタートアップのサービスを楽しんでみた経験で、このようなアイデアを思いつくことができた。

「既存にも月世のカード決済が不可能なわけではありませんでした」。キム・ギテ代表によると、既存には賃貸人が直接カード機を持って決済を受けたり、書面で同意してくれた賃貸人に限って金融会社の革新金融サービスで進行することができた。だが「居住中の家賃家主の年勢が90代だ。これを容易に理解できない」とし、賃貸人非介入型構造の効果性を説明した。集業ペイはPG社を中間に挟み、テナントの送金を代わりに処理する仕組みだ。

「ユーザーは集業で本人の賃貸借契約書を認証し、家賃をカードで決済します。 月税金額でカード実績を積むことはもちろん、ポイントや決済日調整などのカード特典に税額控除、住居・ライフスタイルメンバーシップの恩恵も一緒に享受できます。

平均年齢26.8歳、2030世代が急速に反応

執業ペイユーザーの平均年齢は26.8歳です。多様なカード使用に馴染み、各種特典に敏感な世代だ。キム・ギテ代表は「自然にそうなった」とした。 「既成世代は、家賃を現金で払うのが当然だと思うが、若い世代は「なぜ月税納付だけ現金でなければならない」と疑問を抱いているんです。」

マーケティングは容易ではなかった。 「カードで家賃を出す」という概念がまだ見慣れていて、ぎこちないという人々がまだ多い。一部は「カードカン」と混同する否定的な認識を持つこともある。それでセキュリティと安定性の確保に集中した。デブディは業界で初めてISO 9001とISO 27001を同時に獲得し、安定的で信頼できるサービス運営体系を備えた。

チャーター詐欺防止から家賃金融まで

執業ペイは最初から主力事業ではなかった。集業の統合サービス戦略は、一人世帯が住宅生活で経験する破片化された問題を一つのプラットフォームで解決しようという哲学から出発した。取締役の準備から仕上げまで、全過程を管理できる「引越プランナー」とパーソナライズされた売り物探索機能から始め、以後チャーター詐欺予防のための「チャーター安全レポート」、1人世帯特化情報を盛り込んだ「マガジン」などに範囲を拡張してきた。

「ユーザーが取締役に関わる全過程でいろいろ助けを受けたいと思っていることがわかりました。家の救いや契約書の検討、引越しの準備、そして毎月の月間賭けまで。この中でも特に月税が繰り返し、不便さが大きかったです。だからここに集中することになりました」

収益モデルは3つ、データコラボレーションが核心

こうした1世帯トータルオールインワンサービスを目指す集業の収益源は3つある。カード決済手数料や引越し・清掃・修理など住居関連提携サービス収益、そして金融機関協業を通じた提携カード及びカスタマイズ型金融商品で発生する収益だ。

彼は「複数の金融機関とのコラボレーションを通じて、一人世帯に特化した金融商品を拡張中」と説明した。

「昨年、ハナ銀行、ハナカードとコラボレーションを行いました。ハナカードは提携カードを設計して作ったりしました」

今年はウリ金融グループとカカオバンク、BNK慶南銀行などオープンイノベーション事業を進行して多様な形態のコラボレーションを進めている。

キム・ギテ代表は集業のビジョンを「月世を単純な支出ではなく、個人の金融生活を始める第一歩に変えること」とした。毎月繰り返される月税納付を固定費だけで認識するのではなく、信用度管理、ポイント積立、投資連携など多様な金融特典と連結し、賃借人財務設計と金融ポートフォリオ拡張を可能にする仕組みを目指す。一人世帯が住宅費支出でも実質経済的利益を得ることができるように助けることが方向である。

金融会社ではないが、デブディはユーザーの立場で金融を容易に作ろうとする。技術は人々の日常のお金の流れをより柔軟に変えることに焦点を当てている。

月世のカード決済が常識である世界

類似サービスを繰り広げる他社については「集業ペイの差別化された強みがある」と強調した。業界最低水準の手数料と金融券提携カード、住居生活全般を合わせるメンバーシップサービスなどの恩恵により、ユーザーにより良い選択肢と価値を提供する。

彼は「月税をカードで支払うという概念は慣れていないが、今や資金管理手段として関心を持つ人々が増えている」とし「集業ペイで月世家具が住宅費支出で多様な金融利益を作るのを助けたい」と話した。

家賃を「現金だけ」出した時代は、徐々に暮らしているようだ。

キム・ギテデブディ代表は英国The University of Sheffieldを卒業し、英国でAIベースのコマーススタートアップDiversiTeaを創業した。その後、ソーシャルベンチャーアクセラレータアンダードッグスでコーチとして活動し、様々な創業チームを指導した。 2022年にデブディを創業し、「集業xをローンチした後、現在まで4万人以上のユーザーを確保した。

金基泰代表让“不用房东,刷卡付房租”成为现实

“只有月租不能用信用卡支付,这不是很奇怪吗?”

汝矣岛站前的一家咖啡馆。Devdi的代表金基泰(32岁)比约定时间提前了10分钟到达,他正打开笔记本电脑,聚精会神地思考着什么。“今天早上有新的合作。”屏幕上显示着每月交易情况的仪表盘。一个数字急剧上升的图表吸引了我的目光。

“即使在六个月前,我也没有想到会有如此程度的增长。说实话,我当时把它当成了我最后的挑战。”

Devdi 的主要服务是其 CEO Kim Ki-tae 创立的“Zipup”应用内的月租卡支付解决方案,该应用是一款面向单身家庭的一体化解决方案。这项服务是他在考虑该应用 2023 年上线后如何盈利时构思出来的。自去年 10 月上线以来,Zipup Pay 的月交易额在过去六个月里增长了 150%。

长期独居发现的创业动机

当被问及为什么用卡支付房租的过程如此困难时,他坦言,“这比我想象的要复杂得多。”

“大多数房东都是个人,由于税务问题,他们不愿意接受信用卡付款。”最终,租户必须每月支付现金,而这个过程并没有任何好处。

金基泰代表在异国他乡独自生活了十多年,也曾有过同样的经历。“如果交房租的日子和信用卡扣款的日子重合,或者突然有一笔大额支出,我的钱就很难管理。每次我都会想,‘如果像信用卡一样,付款日期和提款日期之间能留出一些时间就好了。’”

金基泰代表表示,自己在英国创立AI茶饮策划初创公司“DiversiTea”的经验是解决问题的关键。“即使是看似不可能的问题,只要分解成几个步骤就能解决。” 特别是,他之所以能想到这个点子,是源于自己曾使用过Monzo、Revolut、Wise等先进金融科技初创公司的服务。

“以前用卡支付房租并非不可能。”金基泰首席执行官表示,此前房东可以通过刷卡机直接收款,或者只有获得书面同意的房东才能使用金融机构的创新金融服务。然而,他解释了这种不涉及房东的结构的有效性,并表示:“目前每月支付房租的房东已经90多岁了。他们很难理解这一点。” Zipup Pay是一种通过PG公司代为处理租户汇款的结构。

用户在家中验证租赁协议,并使用银行卡支付月租。除了每月支付租金累积卡片性能外,他们还可以享受积分和付款日期调整、税收减免以及住房/生活方式会员福利等卡片优惠。房东仍按月收取租金。

平均年龄26.8岁,2030一代反应迅速

Zipup Pay 用户的平均年龄为 26.8 岁。他们是习惯使用各种银行卡、对各种优惠敏感的一代。首席执行官金基泰表示:“这很自然。” “老一辈人认为用现金支付月租很正常,但年轻一代却感到疑惑:‘为什么月租只能用现金支付?’”

市场营销并非易事。很多人对“刷卡付房租”的概念仍然感到陌生,觉得很别扭。有些人对此持有负面看法,将其与“信用卡诈骗”混淆。因此,我们专注于确保安全性和稳定性。Devdi 在业内率先同时获得 ISO 9001 和 ISO 27001 认证,建立了稳定可靠的服务运营体系。

从防止欺诈到每月租金融资

Zipup Pay并非从一开始就是主营业务。Zipup的整合服务战略始于通过单一平台解决单身家庭居住生活中遇到的碎片化问题。最初,Zipup推出了能够管理从搬家准备到完成整个流程的“搬家规划师”和个性化的房源搜索功能,之后又扩展至预防租房欺诈的“租房安全报告”以及专门针对单身家庭信息的“杂志”。

我们发现用户需要搬家各个方面的帮助。从找房子、审查合同、准备搬家,到支付月租。其中,月租的支付尤其重复且不方便。因此,我们专注于此。

盈利模式有三种,数据协作是关键。

这项一户一站式服务的收入来源包括三个方面:卡支付费用、搬家、清洁和维修等与住房相关的附属服务的收入、以及通过与金融机构合作而获得的附属卡和定制金融产品的收入。

他解释道:“我们正在通过与各金融机构合作,扩大针对单人家庭的金融产品。”

“去年,我们与韩亚银行和韩亚卡合作。韩亚卡还设计并制作了一张合作卡。”

今年,我们正在与友利金融集团、Kakao银行、BNK庆南银行等开展开放式创新项目,并开展各种形式的合作。

首席执行官金基泰表示,公司的愿景是“将每月租金从一项简单的支出转变为开启个人财务生活的第一步”。公司不会将每月租金视为固定成本,而是致力于将其与信用管理、积分累积和投资联动等各种金融福利挂钩,从而实现租户财务规划和金融投资组合的扩展。目标是帮助单身家庭从住房支出中获得真正的经济效益。

Devdi 虽然不是一家金融公司,但其目标是让用户的金融体验更加便捷。该公司的技术致力于让人们日常生活中的资金流动更加灵活。

用信用卡支付房租已成为常识的世界

对于其他提供类似服务的公司,他强调“Zipup Pay拥有差异化优势”,通过业内最低佣金、金融行业附属卡、覆盖住宅生活方方面面的会员服务等优势,为用户提供更好的选择和价值。

他说道:“用卡支付房租的概念并不为人熟知,但越来越多的人开始对其感兴趣,将其作为一种管理财务的方式”,“我想通过 Zipup Pay 帮助租房者从住房支出中获得各种经济利益”。

看来,“仅以现金”支付月租的时代正在慢慢结束。

Devdi 首席执行官金基泰毕业于英国谢菲尔德大学,并在英国创立了人工智能商业初创公司 DiversiTea。之后,他曾在社会创业加速器 Underdogs 担任教练,指导过多个创业团队。自 2022 年创立 Devdi 并推出“Zipupx”以来,该公司迄今已拥有超过 4 万名用户。

Le PDG Kim Ki-tae fait de l'impossible « payer le loyer par carte sans propriétaire » une réalité

« N’est-il pas étrange que seul le loyer mensuel ne puisse pas être payé par carte de crédit ? »

Un café devant la gare de Yeouido. Kim Ki-tae (32 ans), PDG de Devdi, arrivé 10 minutes plus tôt que prévu, était concentré sur quelque chose, son ordinateur portable ouvert. « Un nouveau partenariat est arrivé ce matin. » Un tableau de bord affichant l'état des transactions mensuelles s'affichait à l'écran. Un graphique avec des chiffres en forte hausse a attiré mon attention.

Il y a encore six mois, je ne m'attendais pas à une telle croissance. Pour être honnête, je voyais cela comme mon dernier défi.

Le service principal de Devdi, fondé par son PDG Kim Ki-tae, est la solution de paiement mensuel par carte de loyer intégrée à l'application « Zipup », une solution tout-en-un destinée aux ménages individuels. Ce service a été imaginé par Kim Ki-tae alors qu'il envisageait de le monétiser après le lancement de l'application en 2023. Depuis son lancement en octobre dernier, Zipup Pay a enregistré une croissance de 150 % du montant de ses transactions mensuelles au cours des six derniers mois.

Motivation pour démarrer une entreprise découverte en vivant seul à long terme

Lorsqu’on lui a demandé pourquoi le processus de paiement du loyer par carte était difficile, il a avoué : « C’est plus compliqué que je ne le pensais. »

« La plupart des propriétaires sont des particuliers et hésitent à accepter les paiements par carte pour des raisons fiscales. » Au final, les locataires doivent envoyer de l'argent liquide chaque mois, ce qui n'apporte aucun avantage.

Le PDG Kim Ki-tae a vécu la même expérience lorsqu'il a vécu seul à l'étranger pendant plus de dix ans. « Lorsque le jour où je devais payer mon loyer coïncidait avec celui du prélèvement sur ma carte de crédit, ou lorsque j'avais une grosse dépense soudaine, j'avais du mal à gérer mon argent. À chaque fois, je me disais : "Ce serait plus simple s'il y avait un délai entre la date de paiement et la date de retrait, comme avec une carte de crédit." »

Le PDG Kim Ki-tae a déclaré que son expérience, acquise lors de la création de la startup britannique de sélection de thés par IA « DiversiTea », a été la clé de la résolution du problème. « Même les problèmes qui semblent insolubles peuvent être résolus en les décomposant en étapes. » Cette idée lui est notamment venue de son expérience auprès de startups fintech de pointe telles que Monzo, Revolut et Wise.

« Avant, payer son loyer par carte n'était pas impossible. » Selon le PDG Kim Ki-tae, auparavant, les propriétaires pouvaient recevoir leurs paiements directement via un terminal de paiement, ou seuls ceux ayant donné leur consentement écrit pouvaient utiliser les services financiers innovants des institutions financières. Cependant, il a expliqué l'efficacité d'une structure sans implication des propriétaires : « Le propriétaire actuel qui paie son loyer mensuel a plus de 90 ans. C'est difficile pour eux de comprendre cela. » Zipup Pay est une structure qui traite les paiements des locataires en leur nom en intervenant auprès d'une société de gestion de patrimoine.

Les utilisateurs authentifient leur contrat de location sur place et règlent leur loyer mensuel avec une carte. Outre le cumul des performances de la carte avec le montant du loyer mensuel, ils bénéficient d'avantages tels que des points, des ajustements de date de paiement, des déductions fiscales et des avantages liés à l'adhésion au programme Logement/Art de vivre. Le propriétaire perçoit le loyer mensuel comme auparavant.

Âge moyen 26,8 ans, la génération 2030 réagit rapidement

L'âge moyen des utilisateurs de Zipup Pay est de 26,8 ans. Il s'agit d'une génération habituée à utiliser différentes cartes et sensible aux différents avantages. Le PDG Kim Ki-tae a déclaré : « C'est arrivé naturellement. » « La génération plus âgée pense qu'il est naturel de payer son loyer mensuel en espèces, mais la jeune génération se demande : "Pourquoi ne payer que le loyer mensuel en espèces ?" »

Le marketing n'a pas été simple. Nombreux sont ceux qui ne connaissent pas encore le concept de « paiement du loyer par carte » et le trouvent gênant. Certains ont une perception négative de ce concept, le confondant avec une « fraude à la carte ». Nous avons donc mis l'accent sur la sécurité et la stabilité. Devdi a été le premier du secteur à obtenir simultanément les certifications ISO 9001 et ISO 27001, et a mis en place un système d'exploitation de services stable et fiable.

De la prévention de la fraude au financement mensuel des loyers

Zipup Pay n'était pas l'activité principale dès le départ. La stratégie de services intégrés de Zipup reposait sur la philosophie de résoudre les problèmes fragmentés rencontrés par les ménages monoparentaux sur une plateforme unique. Elle a débuté avec le « Planificateur de déménagement », capable de gérer l'intégralité du processus, de la préparation à la finalisation du déménagement, et la fonction de recherche de logement personnalisée. Le champ d'application a ensuite été élargi pour inclure le « Rapport de sécurité locative » afin de prévenir la fraude locative, et le « Magazine », contenant des informations spécialisées pour les ménages monoparentaux.

Nous avons constaté que les utilisateurs souhaitaient être accompagnés dans tous les aspects de leur déménagement : de la recherche d'un logement à la vérification des contrats, en passant par la préparation du déménagement et le paiement du loyer mensuel. Parmi ces aspects, le loyer mensuel était particulièrement répétitif et contraignant. C'est pourquoi nous avons concentré nos efforts sur ce point.

Il existe trois modèles de revenus et la collaboration en matière de données est essentielle.

Les sources de revenus de ce service tout-en-un pour un ménage d'une personne sont triples : les frais de paiement par carte, les revenus provenant des services affiliés liés au logement tels que le déménagement, le nettoyage et les réparations, et les revenus provenant des cartes affiliées et des produits financiers personnalisés grâce à la collaboration avec les institutions financières.

« Nous développons des produits financiers adaptés aux ménages d’une seule personne grâce à une collaboration avec diverses institutions financières », a-t-il expliqué.

L'année dernière, nous avons collaboré avec Hana Bank et Hana Card. Hana Card a également conçu et créé une carte partenaire.

Cette année, nous menons des projets d’innovation ouverte avec Woori Financial Group, Kakao Bank et BNK Gyeongnam Bank, et mettons en œuvre diverses formes de collaboration.

Kim Ki-tae, PDG de l'entreprise, a déclaré que la vision de l'entreprise est de « transformer le loyer mensuel d'une simple dépense en une première étape vers une vie financière personnelle ». Plutôt que de considérer le loyer mensuel comme un coût fixe, l'entreprise souhaite l'associer à divers avantages financiers tels que la gestion du crédit, l'accumulation de points et l'investissement, afin de permettre la planification financière des locataires et l'expansion de leur portefeuille financier. L'objectif est d'aider les ménages monoparentaux à tirer de réels avantages économiques de leurs dépenses de logement.

Bien qu'il ne s'agisse pas d'une société financière, Devdi vise à simplifier la gestion financière des utilisateurs. Sa technologie vise à fluidifier les flux financiers au quotidien.

Un monde où payer son loyer par carte de crédit relève du bon sens

Concernant les autres entreprises proposant des services similaires, il a souligné que « Zipup Pay possède un atout distinctif. » Elle offre de meilleurs choix et une meilleure valeur ajoutée aux utilisateurs grâce à des avantages tels que les commissions les plus basses du secteur, des cartes affiliées au secteur financier et des services d'adhésion couvrant tous les aspects de la vie privée.

Il a déclaré : « Le concept de payer le loyer avec une carte n'est pas familier, mais de plus en plus de personnes s'y intéressent comme moyen de gérer leurs finances » et « Je veux aider les locataires à générer divers avantages financiers à partir de leurs dépenses de logement grâce à Zipup Pay. »

Il semble que l’ère du paiement mensuel du loyer « uniquement en espèces » touche lentement à sa fin.

Kim Ki-tae, PDG de Devdi, est diplômé de l'Université de Sheffield au Royaume-Uni et a fondé DiversiTea, une startup britannique spécialisée dans le commerce basé sur l'IA. Il a ensuite travaillé comme coach chez Underdogs, un accélérateur de startups sociales, et encadré diverses équipes de startups. Depuis la création de Devdi en 2022 et le lancement de « Zipupx », l'entreprise a conquis plus de 40 000 utilisateurs à ce jour.

You must be logged in to post a comment.